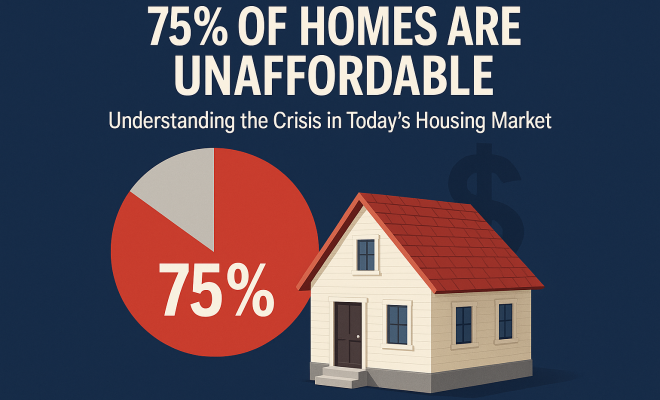

75% of Homes Are Unaffordable: Understanding the Crisis in Today’s Housing Market

“`html

The current real estate landscape in the United States is creating a wave of concern as a staggering 75% of homes for sale are now deemed unaffordable to the average household. This revelation, highlighted in a recent analysis by Bankrate and reported by Axios, has stirred significant conversation around the persistent issue of housing affordability. With median home prices soaring to around $435,000, the financial strain is evident. It’s estimated that a typical household would require an annual income of about $113,000 to comfortably afford a home at this price point. In stark contrast, the median U.S. household income hovers around $80,000, illustrating a troubling disconnect between wages and housing costs.

1. The Current State of the Housing Market: An Overview

To better understand the implications of this shocking statistic, let’s take a closer look at the housing market’s current state. Amid rising interest rates and inflationary pressures, the affordability of housing has plummeted. As interest rates increase, monthly mortgage payments rise, driving many potential buyers out of the market. The Federal Reserve’s aggressive stance on interest rates, aimed at combating inflation, has significantly contributed to this shift. As a result, homebuyers are feeling squeezed tighter than ever as their purchasing power diminishes.

In addition, the pandemic has caused shifts in housing demand, creating imbalances that further complicate the market. Many urban dwellers sought more spacious homes in suburban areas, leading to skyrocketing prices in previously affordable regions. The competition has intensified, leaving many individuals and families frustrated and disillusioned. With over three-quarters of homes out of reach, a sense of urgency is palpable, and the term “unaffordable housing market” has become a recurring theme in discussions about housing.

2. The Income-Housing Cost Gap: A Closer Look

The crux of the issue lies in the disparity between income levels and housing costs. A typical household earning around $80,000 annually faces a daunting challenge when trying to afford a home priced at $435,000. The Bankrate analysis underscores this gap, revealing that households would need to earn at least $113,000 to afford the median home without stretching their finances too thin. This significant income gap not only poses a barrier for first-time homebuyers but also impacts renters and lower-income households.

This discrepancy has far-reaching implications. As homeownership becomes less attainable, more individuals are pushed into the rental market, exacerbating rental demand and potentially driving up prices in that sector as well. Furthermore, the pressure on affordable housing options can lead to increased overcrowding and housing instability for lower-income families. According to the National Low Income Housing Coalition, there is a severe shortage of affordable rental units, further compounding the housing crisis.

3. Dave Ramsey’s Perspective: A Voice of Concern

Financial expert Dave Ramsey has weighed in on the current housing crisis, labeling it the “most unrealistic real estate market in 100 years.” His assertion is not only a reflection of frustration but also highlights the increasing sense of urgency among financial advisors and economists. Ramsey’s comments resonate with many Americans who feel trapped by the rising costs of homeownership.

Ramsey advocates for financial literacy and prudent financial planning, urging potential homebuyers to evaluate their budgets carefully before committing to large purchases. His perspective sheds light on the importance of approaching the home-buying process with caution and awareness of the broader economic implications. As the crisis unfolds, individuals would do well to heed such advice to avoid the pitfalls of an unaffordable housing market.

4. The Impact of Rising Interest Rates: A Double-Edged Sword

One of the primary factors contributing to the unaffordable housing market is the recent rise in interest rates. In an attempt to combat inflation, the Federal Reserve has implemented a series of interest rate hikes. While this may be a necessary step from an economic standpoint, it has created additional hurdles for prospective homebuyers.

Higher interest rates mean higher monthly mortgage payments. For instance, on a $400,000 mortgage, a 1% increase in interest can add roughly $400 to the monthly payment. For many families, this extra expense can be the difference between affording a home or renting indefinitely. As a result, potential buyers might find themselves facing a choice: stretch their finances to secure a mortgage or continue renting, which may also see increasing costs.

5. The Role of Supply Chain Issues: Construction Delays

The housing supply has also been affected by various factors, including supply chain disruptions and labor shortages. These issues have delayed construction timelines and increased building costs, exacerbating the unaffordable housing market scenario. As builders struggle to obtain materials and hire skilled labor, the pace of new housing development has slowed significantly. (See: U.S. Census Bureau Housing Statistics.)

With fewer new homes being built, demand continues to outstrip supply, resulting in heightened competition among buyers. This imbalance can drive up home prices even further, adding to the financial strain faced by many. Moreover, the lack of inventory in the housing market fuels the perception of urgency, with potential buyers feeling pressured to make quick decisions before prices escalate further.

6. Regional Disparities in Housing Costs: A Nationwide Concern

The housing affordability crisis isn’t uniform across the United States; it varies significantly by region. Areas such as San Francisco, New York City, and Los Angeles have long been considered unaffordable due to their elevated home prices. However, cities like Austin, Texas, and Boise, Idaho, which were previously seen as affordable, have also witnessed substantial price increases in recent years.

This regional disparity further complicates the housing market, as individuals and families may feel compelled to relocate to areas with lower costs of living. The challenge is that these regions may not have the same job opportunities or amenities, leading to a difficult choice between affordability and quality of life. As remote work gains popularity, the choices of where to live may become more flexible, but the underlying issue of housing affordability remains a significant hurdle.

7. Potential Solutions: Addressing the Crisis

Addressing the unaffordable housing market requires a multifaceted approach involving policymakers, developers, and community stakeholders. Some potential solutions include increasing the supply of affordable housing through incentives for builders, encouraging the development of mixed-income housing, and streamlining the permitting process to expedite construction.

Additionally, government programs aimed at assisting first-time homebuyers can play a crucial role in bridging the gap between income levels and housing costs. Programs providing down payment assistance and low-interest loans can help aspiring homeowners enter the market without overextending their finances. Communities should also consider implementing rent control measures to help stabilize rental markets and protect vulnerable populations.

8. Consumer Awareness: Navigating the Housing Market

In a market where 75% of homes are unaffordable, potential buyers need to approach the housing market with a clear understanding of their financial situation. It’s essential to evaluate what you can realistically afford, factoring in not just the purchase price but also property taxes, maintenance, and insurance costs.

Working with a financial advisor or a knowledgeable real estate agent can provide valuable insights into navigating the current landscape. They can help identify potential neighborhoods that may offer more affordable options or suggest alternative strategies, such as exploring multi-family properties or fixer-uppers. By being informed and proactive, you can better position yourself in this challenging market.

9. The Future of Housing: Trends to Watch

Looking ahead, the future of the housing market remains uncertain. As interest rates and economic conditions continue to evolve, potential buyers will need to stay informed about shifts in the market. Trends such as remote work and demographic shifts can influence housing demand in the coming years, potentially alleviating pressure in certain areas.

Moreover, as policymakers and communities react to the growing crisis, new regulations and initiatives may emerge that could reshape the housing landscape. While the unaffordable housing market poses significant challenges, there is hope that concerted efforts can lead to more accessible options for future homeowners. The key lies in recognizing the urgency of the situation and advocating for solutions that prioritize affordability in housing.

10. Understanding the Broader Economic Impact: Housing’s Role in the Economy

The unaffordable housing market extends beyond individual buyers and renters; it has broader implications for the national economy. Housing is a significant driver of economic activity. When home sales are robust, they contribute to job creation in construction, real estate services, and related sectors. Conversely, when housing becomes unaffordable, it stifles economic growth by limiting consumer spending.

According to a report from the National Association of Realtors, a 10% increase in home prices can reduce the number of home sales by 5%. This reduction not only affects the housing market but also trickles down to various sectors reliant on housing activity. Fewer sales mean less revenue for real estate agents, decreased demand for home goods, and potentially a slowdown in construction jobs. (See: Federal Reserve Monetary Policy Overview.)

11. Social Implications: The Human Cost of Unaffordable Housing

The human cost of the unaffordable housing market often gets overlooked in economic analyses. Many families are forced to make difficult choices due to rising housing costs. For instance, some families may need to allocate a larger portion of their income to housing, leaving less available for other essential expenses like healthcare, education, and groceries.

In extreme cases, unaffordable housing can lead to homelessness. Rising rents and stagnant wages have driven more people into precarious living situations, such as couch surfing or living in their vehicles. The point is clear: unaffordable housing does not just affect financial stability; it impacts people’s lives, health, and well-being.

12. FAQs About the Unaffordable Housing Market

What qualifies as an “unaffordable” home?

A home is typically considered unaffordable when a household spends more than 30% of its gross income on housing costs, including mortgage payments, property taxes, and insurance. The 30% threshold is a widely accepted benchmark for determining housing affordability.

Why are housing costs rising so rapidly?

Several factors contribute to the rapid rise in housing costs, including low inventory, high demand, increasing construction costs, and rising interest rates. The pandemic also shifted housing preferences, with many wanting larger spaces, further driving up prices.

What can I do if I can’t afford a home?

If homeownership seems out of reach, consider renting in a more affordable area while saving for a larger down payment. Look into programs that assist first-time buyers, such as down payment assistance or government loans. You might also explore shared ownership or co-housing as alternatives to traditional home buying.

Are there any government programs to assist with buying a home?

Yes, various government programs exist to assist homebuyers, especially first-time buyers. These include FHA loans, VA loans for veterans, and USDA loans for rural homebuyers. Additionally, many states offer down payment assistance programs that can help bridge the gap for buyers struggling to make a full down payment.

How do rising interest rates affect my mortgage?

Rising interest rates lead to higher mortgage rates, which increases the monthly payment for borrowed funds. Higher payments can make homeownership less affordable, discouraging many potential buyers from entering the market. If you’re in the market for a home, it’s essential to lock in a rate as soon as possible to avoid higher costs.

Is it a good time to buy a home despite high prices?

Whether it’s a good time to buy depends on your personal situation. If you’re financially stable, have a steady income, and plan to stay in one location for several years, buying might be a worthwhile investment despite current prices. However, if you’re uncertain about employment or may need to move soon, it might be wiser to wait.

13. Housing Market Predictions: What Experts Say

Many real estate experts are weighing in on the future of the housing market. Predictions vary, but several trends are emerging. For instance, some analysts believe that as interest rates stabilize, the housing market may start to cool, allowing prices to level off or even decrease. Others argue that the fundamental supply-demand imbalance will keep prices elevated in many regions. (See: U.S. Department of Housing and Urban Development.)

A recent survey by the National Association of Realtors noted that while many buyers are currently sidelined due to high costs, interest in homeownership remains strong. Nearly 60% of potential buyers expressed a willingness to purchase a home, suggesting that when conditions improve, demand could rebound quickly.

14. Comparing Urban and Suburban Markets: Shifting Preferences

The pandemic has prompted a notable shift in housing preferences between urban and suburban areas. As remote work policies became more common, many families opted to leave densely populated cities for suburban or rural areas, seeking more space and affordable pricing. This trend has fueled price increases in suburban markets that were once considered affordable.

In contrast, some urban areas have experienced a decrease in demand, leading to a softening of prices. For example, cities like New York and San Francisco saw rental prices dip as people moved away. However, as cities begin to recover and remote work policies evolve, it’s unclear if these trends will persist or if urban areas will regain their appeal.

15. Global Perspectives on Housing Affordability: Lessons from Abroad

The issue of housing affordability is not unique to the United States; many countries face similar challenges. For instance, in Canada, the federal government has implemented various strategies to tackle affordability, including a national housing strategy aimed at reducing homelessness and increasing the supply of affordable housing.

Germany offers lessons in how to manage housing affordability through long-term rental contracts and robust tenant protections. By ensuring that rental prices remain stable and providing security to renters, Germany has managed to maintain a more balanced housing market. Observing these international approaches could provide valuable insights into addressing the housing crisis in the U.S.

16. Future Innovations in Housing: What’s on the Horizon?

The housing market may also benefit from innovative approaches to construction and development. For example, modular and prefabricated homes are gaining traction as cost-effective alternatives to traditional building methods. These techniques can significantly reduce construction time and costs, potentially leading to more affordable housing options.

Additionally, advancements in technology, such as smart home features and energy-efficient appliances, can lower long-term living costs and make homes more appealing to buyers. The integration of sustainable building practices can also play a critical role in addressing the affordability crisis while promoting environmental responsibility.

“`

Trending Now

- our breakdown of the fragmenting digital economy: who will thrive in global competition?

- How Two Entrepreneurs Turned a Simple…

- the complete explanation

- this guide on why medicare advantage enrollment is surging in 2026: the numbers you need to know

- our breakdown of why erectile dysfunction peaks in winter: unpacking the seasonal puzzle

Frequently Asked Questions

What percentage of homes are considered unaffordable?

Currently, 75% of homes for sale in the United States are deemed unaffordable for the average household, highlighting a significant crisis in housing affordability.

What is the average income needed to afford a home?

To comfortably afford a median-priced home, which is around $435,000, a typical household would require an annual income of approximately $113,000.

How have rising interest rates affected the housing market?

Rising interest rates have led to increased monthly mortgage payments, making it more difficult for potential buyers to enter the market and exacerbating the affordability crisis.

What factors are contributing to the housing affordability crisis?

Key factors include soaring median home prices, rising interest rates, inflationary pressures, and shifts in housing demand due to the pandemic, all contributing to the affordability crisis.

Why are urban dwellers moving to suburban areas?

Many urban dwellers are seeking more spacious homes in suburban areas due to changing preferences during the pandemic, which has resulted in increased competition and rising prices in those regions.

Agree or disagree? Drop a comment and tell us what you think.