Why Apple’s Pay Later Feature Could Be Bad News for Affirm and Klarna

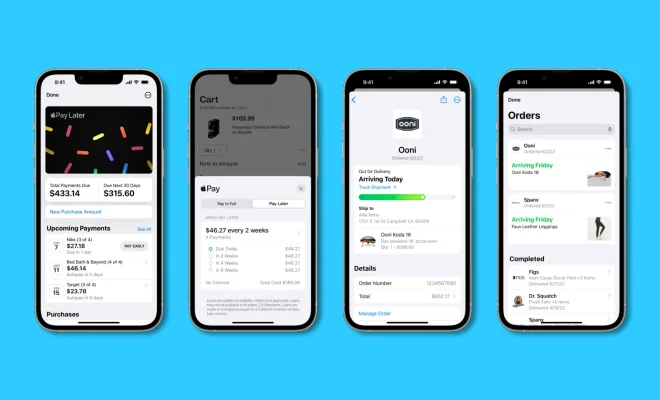

Apple has recently launched its Pay Later feature, which allows users to split their purchases into four interest-free payments over time. While this may seem like good news for Apple users, it could spell bad news for Affirm and Klarna, two buy now, pay later (BNPL) companies that are popular in the market.

BNPL companies have become increasingly popular in recent years, particularly with younger consumers. These companies offer an alternative to traditional credit cards, with the promise of no interest charges and flexible repayment options. Affirm and Klarna are two of the biggest players in this lucrative market, but Apple’s entry into the fray could shake things up significantly.

One of the biggest advantages that Apple has over Affirm and Klarna is its existing customer base. Apple has a huge and loyal customer base, and many of these customers may be tempted to use the Pay Later feature rather than sign up for a new BNPL service. In addition, Apple’s Pay Later option is integrated into the company’s ecosystem, making it easier for users to complete their purchases seamlessly.

Another advantage that Apple has over its rivals is brand recognition. Apple is one of the most recognized brands in the world, and many consumers trust the company implicitly. This could make users more likely to choose Apple over another BNPL service, particularly if they are already using other Apple products.

One potential disadvantage for Affirm and Klarna is that Apple’s Pay Later feature is interest-free. While this may be good news for Apple users, it could make it harder for BNPL companies to compete. Affirm and Klarna both make money by charging interest on their loans, so the lack of interest on Apple’s Pay Later feature could make it harder for these companies to attract customers.

Finally, Apple’s Pay Later feature is limited to purchases made through the company’s own retail stores and online store. This means that other retailers will not be able to offer the feature to their customers, which could limit its adoption. However, Apple is likely to expand the Pay Later feature to other merchants in the future, which could make it a more serious threat to Affirm and Klarna.

In conclusion, Apple’s Pay Later feature is likely to be bad news for Affirm and Klarna, as it offers several advantages over these BNPL companies. Apple already has a huge customer base and a strong brand, which could make it harder for Affirm and Klarna to compete. In addition, the lack of interest on Apple’s Pay Later feature could make it less attractive for consumers to switch to another BNPL service. Overall, Affirm and Klarna will need to step up their game if they want to compete with Apple’s latest offering.