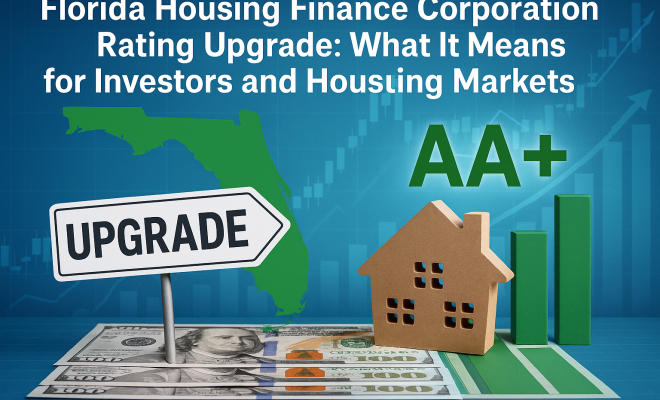

Florida Housing Finance Corporation Rating Upgrade: What It Means for Investors and Housing Markets

“`html

The recent upgrade of the Florida Housing Finance Corporation’s issuer rating by Moody’s to Aa3 from A1 marks a significant turning point for the state’s housing finance landscape. This upgrade, coupled with a revised outlook to stable, reflects enhanced credit strength for the housing finance issuer and is a pivotal moment for bond investors tracking municipal debt. In this article, we will delve into the implications of this rating upgrade, the broader context of Florida’s housing market, and what this means for investors and stakeholders.

Understanding the Rating Upgrade

Moody’s Investors Service is one of the leading credit rating agencies, providing insights into the creditworthiness of various entities, including municipalities and housing finance authorities. The rating upgrade from A1 to Aa3 suggests a stronger ability to meet financial commitments. But what exactly does this mean?

The upgrade indicates that the Florida Housing Finance Corporation (FHFC) has improved its financial health, effectively enhancing its ability to manage risks associated with housing finance. In practical terms, a higher rating typically signals lower risk to investors, which can lead to reduced borrowing costs for the state’s housing initiatives. This is critical in a period when housing affordability is a pressing issue nationwide.

Impact on Investors

For bond investors, the Florida Housing Finance Corporation rating upgrade holds several implications. Firstly, higher ratings often lead to a decrease in yields on bonds issued by the entity, as investors are generally willing to pay a premium for lower-risk securities. This could result in improved portfolio valuations for those holding FHFC bonds.

Moreover, a stable outlook suggests that the FHFC is likely to maintain its improved credit strength over the near term, which can provide investors with confidence. This type of stability is essential in municipal finance, where fluctuations in interest rates and credit ratings can significantly impact investment strategies.

The Broader Picture: Housing Markets in Florida

The upgrade of the FHFC’s rating is particularly significant in the context of Florida’s housing market. In recent years, Florida has experienced a dramatic increase in housing prices, driven by factors such as population growth, low-interest rates, and a robust job market. According to recent statistics from the Florida Association of Realtors, the median home price in Florida has surged, making affordability a critical issue for many residents.

Given this backdrop, the FHFC plays a vital role in supporting affordable housing initiatives across the state. With an enhanced credit rating, the corporation can issue bonds at more favorable rates, which can be used to finance affordable housing projects, thereby addressing the growing demand for housing options in Florida.

How Rating Changes Influence Municipal Debt

Rating changes, like the Florida Housing Finance Corporation rating upgrade, are crucial in the realm of municipal debt. When an issuer receives a higher rating, it fundamentally alters the landscape for future borrowing. Lower borrowing costs can lead to increased investment in public projects and services, ultimately benefiting the community.

Conversely, should an issuer experience a rating downgrade, the implications can be severe. Increased borrowing costs can stifle growth, limit public services, and reduce the quality of life in affected areas. As such, the FHFC’s upgrade is a positive development not just for the corporation but for the many communities it serves. (See: U.S. Department of Housing and Urban Development.)

Investor Sentiment and Market Reactions

Investor sentiment tends to react swiftly to credit rating changes. When news of the FHFC’s upgrade broke, it likely sparked interest among investors focusing on municipal bonds and housing-related securities. Increased demand for bonds from a newly upgraded issuer can lead to a reduction in yields, which is beneficial for existing bondholders.

Moreover, investors seeking yield in an uncertain market may view the FHFC’s bonds as an attractive opportunity, particularly given the backdrop of rising interest rates in other sectors. The overall sentiment around housing finance can also be influenced by broader economic conditions, including inflation rates, employment figures, and state-level economic growth.

The Role of the Florida Housing Finance Corporation

Established in 1980, the Florida Housing Finance Corporation has been instrumental in providing affordable housing solutions across the state. The organization primarily functions by issuing tax-exempt bonds, which fund various housing programs aimed at assisting low- and moderate-income Floridians.

Through partnerships with local governments, non-profit organizations, and private developers, the FHFC has played a crucial role in expanding the availability of affordable housing in Florida. The recent upgrade in its credit rating amplifies its capacity to fulfill its mission more effectively.

Historical Context of Housing Finance Ratings

The landscape of housing finance ratings has evolved dramatically over the years, particularly post-financial crisis. Prior to the 2008 housing market collapse, many municipal housing issuers received favorable ratings even when financial conditions were tenuous. However, the crisis led to more stringent rating methodologies and increased scrutiny of housing finance entities.

In the wake of these changes, credit rating agencies, including Moody’s, have developed more robust frameworks for evaluating issuer creditworthiness. The recent upgrade of the FHFC may be a reflection of these evolving methodologies, as well as improved economic conditions in Florida.

Challenges Ahead for Florida’s Housing Market

While the FHFC’s rating upgrade is a positive sign, challenges remain for Florida’s housing market. The state continues to grapple with issues such as housing supply shortages, rising construction costs, and regulatory hurdles that affect new development.

Given the surge in demand for affordable housing, the FHFC must navigate these challenges effectively to maintain its upward trajectory. Moreover, the ongoing inflationary pressures and potential interest rate hikes could impact both the affordability of housing and the corporation’s ability to finance future projects.

Expert Perspectives on the Rating Upgrade

Industry experts have weighed in on the implications of the Florida Housing Finance Corporation rating upgrade. Many view it as a reaffirmation of the state’s commitment to addressing housing affordability and economic development through responsible financial practices.

According to housing finance analysts, the upgrade could serve as a model for other states looking to improve their credit profiles. It demonstrates how effective management of public resources and transparency can lead to improved investor confidence, ultimately resulting in better financial outcomes.

The Economic Impact of Housing Finance Ratings

The economic implications of the Florida Housing Finance Corporation rating upgrade extend beyond the immediate benefits to bond investors. Upgraded credit ratings can stimulate economic growth by attracting investment into the state’s housing sector. As borrowing costs decrease, developers may be more inclined to undertake new projects, leading to job creation and further economic development in surrounding communities.

A study by the National Association of Home Builders found that for every 100 new home construction jobs created, approximately 300 additional jobs are supported in related industries, such as manufacturing and retail. Thus, the FHFC’s improved rating not only benefits investors but also has the potential to ripple through Florida’s economy, creating a more robust job market and enhanced quality of life for residents.

Comparative Analysis with Other States

To understand the significance of the FHFC’s rating upgrade, it is instructive to compare it with other housing finance entities across the nation. States like Texas and California have historically held higher ratings due to their more extensive economic bases and housing markets. However, Florida’s recent upgrade signifies an improvement in its financial management and housing policies, positioning it favorably against these states.

For example, the California Housing Finance Agency (CalHFA) has maintained high ratings but faces challenges related to affordability and homelessness despite its robust rating. In contrast, Florida’s upgrade may reflect a proactive approach to mitigating these issues before they escalate. This comparison highlights the importance of effective housing finance strategies and their impact on state credit ratings.

Future Prospects for the Florida Housing Finance Corporation

The future of the Florida Housing Finance Corporation looks promising, especially with the recent rating upgrade. The corporation is expected to continue leveraging its improved credit rating to secure funding for innovative housing solutions aimed at addressing the needs of a diverse population. Strategies such as public-private partnerships and community land trusts may be employed to maximize the impact of available resources.

Additionally, as the housing crisis continues to evolve, the FHFC’s ability to adapt and implement forward-thinking solutions will be critical. Initiatives focused on sustainable development, affordable housing preservation, and enhancing accessibility will likely play an essential role in the corporation’s future success. These efforts could further entrench the FHFC as a leader in housing finance and development in Florida.

Potential Risks and Considerations

Despite the optimistic outlook, several risks and considerations remain for the Florida Housing Finance Corporation. For instance, the potential for economic downturns or shifts in the real estate market could pose challenges to the corporation’s financial stability. Additionally, changes in federal housing policy or funding could impact the FHFC’s operations and ability to serve its constituents effectively.

Moreover, as the state’s population continues to grow, the demand for affordable housing may outpace supply unless proactive measures are taken. The FHFC will need to monitor these dynamics closely and adjust its strategies accordingly to navigate the complexities of the housing finance environment.

FAQs about the Florida Housing Finance Corporation Rating Upgrade

- What does the upgrade from A1 to Aa3 mean?

It indicates enhanced credit strength and lower risk for investors, resulting in potentially reduced borrowing costs. - How does this affect bond investors?

Investors may see improved portfolio valuations and reduced yields on newly issued bonds. - Why is the FHFC important?

The FHFC plays a critical role in providing affordable housing solutions to low- and moderate-income residents in Florida. - What are the broader implications for Florida’s housing market?

The upgrade can lead to increased funding for affordable housing initiatives, addressing demand amid rising prices. - What challenges does the FHFC face moving forward?

Challenges include housing supply shortages, rising construction costs, and potential impacts from inflation and interest rates. - How does this rating upgrade impact Florida’s economy?

The upgrade may attract more investments in housing, leading to job creation and economic growth across the state. - What are the lessons learned from the FHFC’s experience?

The FHFC’s upgrade highlights the importance of transparent management and proactive housing policies in improving credit ratings. - How does the FHFC compare with housing finance agencies in other states?

While states like California and Texas have strong ratings, Florida’s recent upgrade indicates significant improvements in financial management and housing policy.

The Significance of Municipal Ratings in Housing Accessibility

Municipal credit ratings, such as the upgrade of the FHFC, play a vital role in determining housing accessibility for low- to moderate-income populations. Improved ratings can lead to lower costs of financing, enabling housing programs to serve a greater number of people. For instance, affordable housing projects funded through tax-exempt bonds can offer lower rents, which is crucial for families struggling to make ends meet in a high-cost environment.

Moreover, access to affordable housing positively impacts community stability. Studies show that individuals and families living in stable housing environments are more likely to experience better health outcomes, maintain steady employment, and participate in educational opportunities. Therefore, the FHFC’s rating upgrade is not just a financial milestone; it is a step toward enhancing the quality of life for many Floridians.

Long-Term Housing Affordability Solutions

As Florida’s population continues to grow, creating long-term solutions for housing affordability will be imperative. The FHFC’s improved credit rating presents an opportunity to expand the scope of affordable housing initiatives. Potential strategies include increasing funding for homebuyer assistance programs, enhancing support for rental assistance, and incentivizing developers to build affordable units through tax credits and grants.

Furthermore, the FHFC can engage in strategic partnerships with local governments to develop mixed-income housing projects that integrate affordable units into higher-end developments. This approach not only bolsters housing supply but also promotes economic diversity within communities.

The Role of Technology in Housing Finance

Technology is significantly reshaping the housing finance landscape. The FHFC can leverage innovative technologies to streamline operations, improve data analysis, and enhance stakeholder engagement. For instance, utilizing blockchain technology can increase transparency in financial transactions, while data analytics can provide insights into housing market trends, helping the FHFC make more informed decisions.

Additionally, technology can improve access to affordable housing information for potential renters and buyers. Creating user-friendly online platforms that provide resources, applications, and updates can help demystify the process of obtaining affordable housing, making it more accessible for residents.

Conclusion

In conclusion, the Florida Housing Finance Corporation rating upgrade represents a significant event in the world of municipal finance. It reflects improved credit strength and carries profound implications for investors, housing markets, and the state’s ongoing efforts to address housing affordability. As stakeholders navigate the challenges ahead, the FHFC’s enhanced credit profile may prove invaluable in securing funding and resources necessary to meet Florida’s housing needs. With a commitment to innovation and community-focused solutions, the FHFC is well-positioned to continue playing a pivotal role in shaping the future of housing in Florida.

“`

Trending Now

- our breakdown of unlocking insights: how brand intelligence in 2026 will transform business decisions

- this guide on the alarming truth: how inflation, ai, and supply chains are transforming the economy

- The Google Antitrust Battle: How Default Search Deals Impact Competition and Consumer Choice

- 50 Profitable Freelance Business Ideas to…

- our breakdown of how google’s ai search is transforming saas ppc strategies for startups

Frequently Asked Questions

What does the rating upgrade for Florida Housing Finance Corporation mean?

The upgrade of the Florida Housing Finance Corporation's rating from A1 to Aa3 by Moody's indicates improved financial health and a stronger ability to meet financial commitments, suggesting lower risk for investors and potentially reduced borrowing costs for housing initiatives.

How does a rating upgrade affect bond investors?

A rating upgrade generally leads to lower yields on bonds issued by the entity, as investors prefer lower-risk securities. This can enhance portfolio valuations for those holding Florida Housing Finance Corporation bonds.

What is the significance of a stable outlook for FHFC?

A stable outlook indicates that the Florida Housing Finance Corporation is likely to maintain its improved credit strength in the near term, providing investors with confidence and stability in the municipal finance market.

Why is housing affordability important in the context of this rating upgrade?

The rating upgrade is crucial for enhancing the Florida Housing Finance Corporation's ability to manage risks and reduce borrowing costs, which is vital during a time when housing affordability is a significant issue across the nation.

How does Moody's rating influence municipal debt?

Moody's ratings provide insights into the creditworthiness of entities like the Florida Housing Finance Corporation, influencing investor perceptions and decisions regarding municipal debt, ultimately affecting the cost and availability of financing for housing initiatives.

What did we miss? Let us know in the comments and join the conversation.